Go it alone or take professional guidance ??

Most products are available for you to buy yourself either "over the counter" from financial institutions or over the 'phone from some non-traditional players ( such as supermarkets ) or on what is known as an "execution only" basis. With this approach, you take full responsibility for the suitability (or not !) of the investments for you. This often suits people who like to be very "hands on" and perhaps wanting to actively change / manage their portfolio.

By using a professionally qualified financial adviser (look out for initials such as MLIA or MSFA) you will be provided with a set of recommendations as to the best course of action for you to take. To provide this advice, the consultant will carry out a review of your current financial circumstances, looking at your present and future requirements and only then recommend what you should do. This would vary according to your own individual needs; it may be some insurance plans or a portfolio of different investments.

But aren't financial advisers just commission hungry insurance salesmen ???

In my opinion, no.

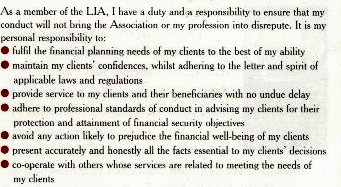

Unlike many other industries, financial planning is highly regulated. Anyone seeking to offer financial advice must, by law, be subject to a number of regulations and checks. For the past couple of years, all advisers (including those who had been in their jobs for 20,30, 40 etc years) have had to demonstrate their technical knowledge and obtain industry standard qualifications. This led to many of the less well intentioned to leave their jobs. Having obtained the new qualification, each adviser is subject to regular ongoing training & development as well as be liable to have the government's regulators apply independant checking of their work. Many also belong to professional bodies with their own codes of conduct. The example below, is the code of the Life Insurance Association which is the largest group of professional advisers in the UK and whose members advise on investments, pensions and savings as well as insurances.

However, also unlike other professions such as, for instance solicitors, most financial consultants are not paid fees by those people seeking their advice. Instead of the customer having to pay, it is the investment or insurance company that pays out for the introduction of the business.

Some people are paid purely on a commission basis; others paid a salary only; some paid a mixture of salary and commission and/or bonuses.

However the remuneration is paid, it should not materially affect the standard of the advice you are given. In each case when advice is given, in order to prove that the product recommended to you is an appropriate one, your adviser will provide you with a document that explains the reasons why it is "best advice" for you. You may rely on this as, if you later have reason to challenge the advice given, the regulatory authorities will examine such papers to see whether you were mis-advised.

In summary, most products can be bought without advice. However, a consultation is usually free and without obligation and you have the opportunity to have an expert sort out your finances for you, without any cost to yourself as someone else is picking up the tab. In my (albeit possibly biased) opinion, you have a lot to gain and nothing much to lose by taking advice rather than dealing with someone over the phone or just filling out a coupon from a newspaper.

Please use your browser's BACK function to return to your previous page